- Honda Motor reported that its global vehicle production fell 5% in February 2026, as output declines in Asia, including a 27% drop in China, outweighed a 9% increase in Japan and growth earlier this year in North America.

- This uneven regional mix highlights Honda’s growing dependence on Japan and North America to offset weaker Asian production, which could affect how investors assess the resilience of its global manufacturing footprint.

- We’ll now examine how February’s weaker Asian output, particularly in China, may influence Honda Motor’s existing investment narrative and risk balance.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Honda Motor Investment Narrative Recap

To own Honda Motor, you need to be comfortable with a global automaker that is rebalancing its production footprint while working through profit pressure in autos and electrification. February’s 5% production decline, driven by a sharp 27% drop in China and broader Asian weakness, reinforces the key near term risk around underperforming Asian volumes. It also puts more weight on the main short term catalyst, which is Honda’s ability to keep North American and Japanese output and mix strong enough to support margins.

The recent guidance cut on March 12, which shifted Honda from a projected operating profit of ¥550,000 million to a forecast operating loss of between ¥570,000 million and ¥270,000 million for FY ending March 2026, is the clearest backdrop to view this production news. The weaker Asian output sits uncomfortably beside already pressured profitability and EV related losses, and keeps attention on how quickly Honda can improve its auto margins while reshaping its electrification plans.

Yet beneath Honda’s production shift, there is a risk that investors should be aware of around prolonged EV losses and regional price competition that could…

Read the full narrative on Honda Motor (it’s free!)

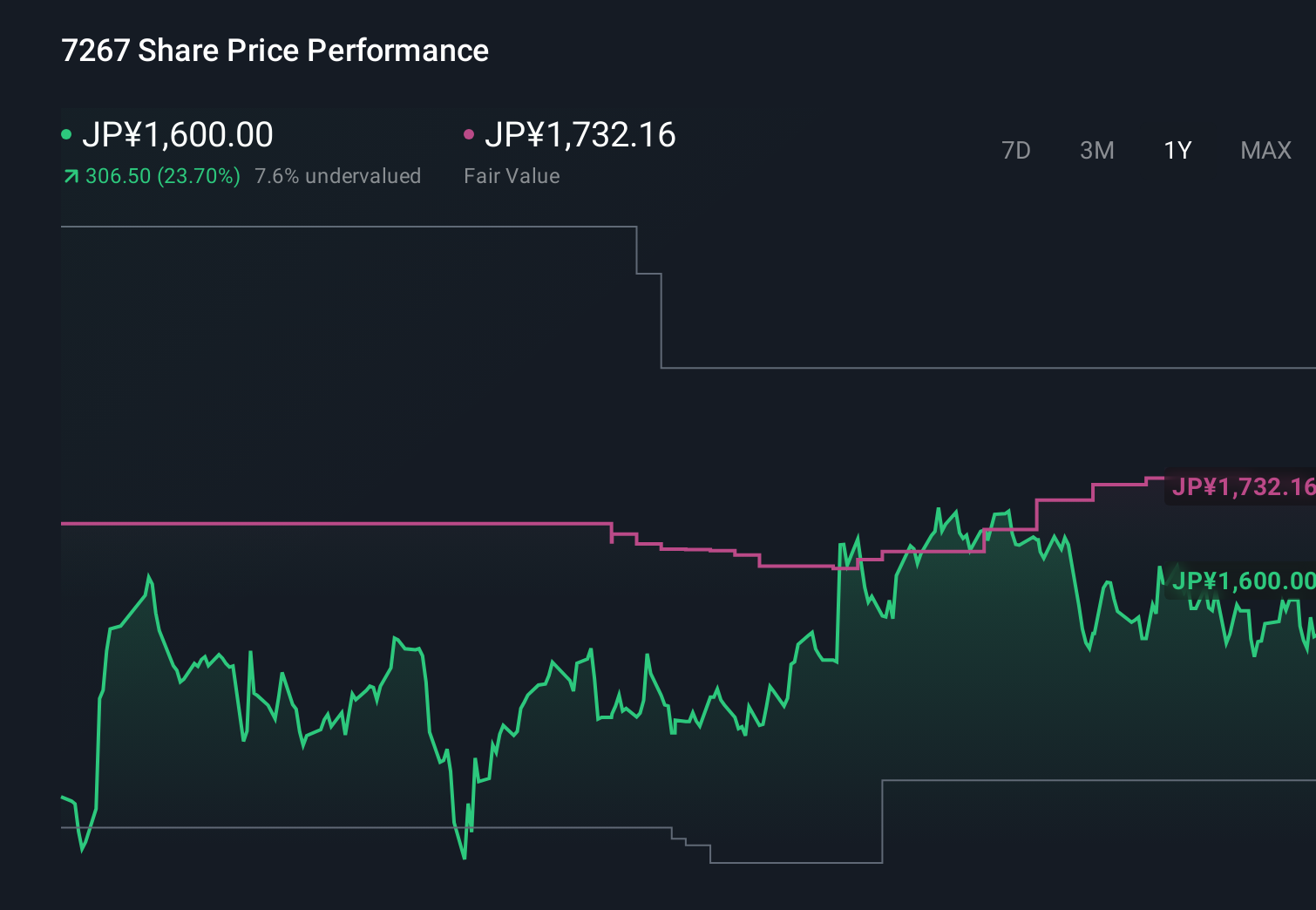

Honda Motor’s narrative projects ¥22,900.1 billion revenue and ¥831.9 billion earnings by 2029. This requires 2.4% yearly revenue growth and about a ¥335.9 billion earnings increase from ¥496.0 billion today.

Uncover how Honda Motor’s forecasts yield a ¥1579 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the lowest analysts were already more pessimistic, assuming revenues around ¥20,942.2 billion and earnings of ¥655.4 billion by 2028, and February’s Asian production slump could reinforce those concerns for you if you worry that weaker EV execution and tariff pressures might weigh on Honda longer than consensus expects.

Explore 2 other fair value estimates on Honda Motor – why the stock might be worth as much as 24% more than the current price!

Reach Your Own Conclusion

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Honda Motor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com