According to Zhitong Finance APP, on April 13, Cui Dongshu, Secretary General of the Passenger Car Association, published an article analyzing the trends in the automobile sub-market and the competitive performance of manufacturers in March 2026. China’s macroeconomy maintained robust growth, and driven by national promotional policies, the automotive market experienced strong expansion. In 2025, the overall national automotive market performed strongly, with significant recovery in the truck and bus markets. Due to the exceptionally strong policy support last year, there was a noticeable contraction in policies in 2026, leading to continued negative retail growth for passenger vehicles from January to March this year. However, due to increased exports, manufacturer sales growth remained relatively stable in March. The performance of new energy vehicles in March was not particularly strong, but the export market for automobiles remained robust. There was little change in manufacturers’ inventories, and the usual end-of-quarter inventory pressure did not occur. The commercial vehicle market in 2026 showed structural growth driven by equipment renewal subsidies, accelerating electrification in logistics and transportation sectors thanks to high subsidies, and the commercial vehicle sector exhibited high activity.

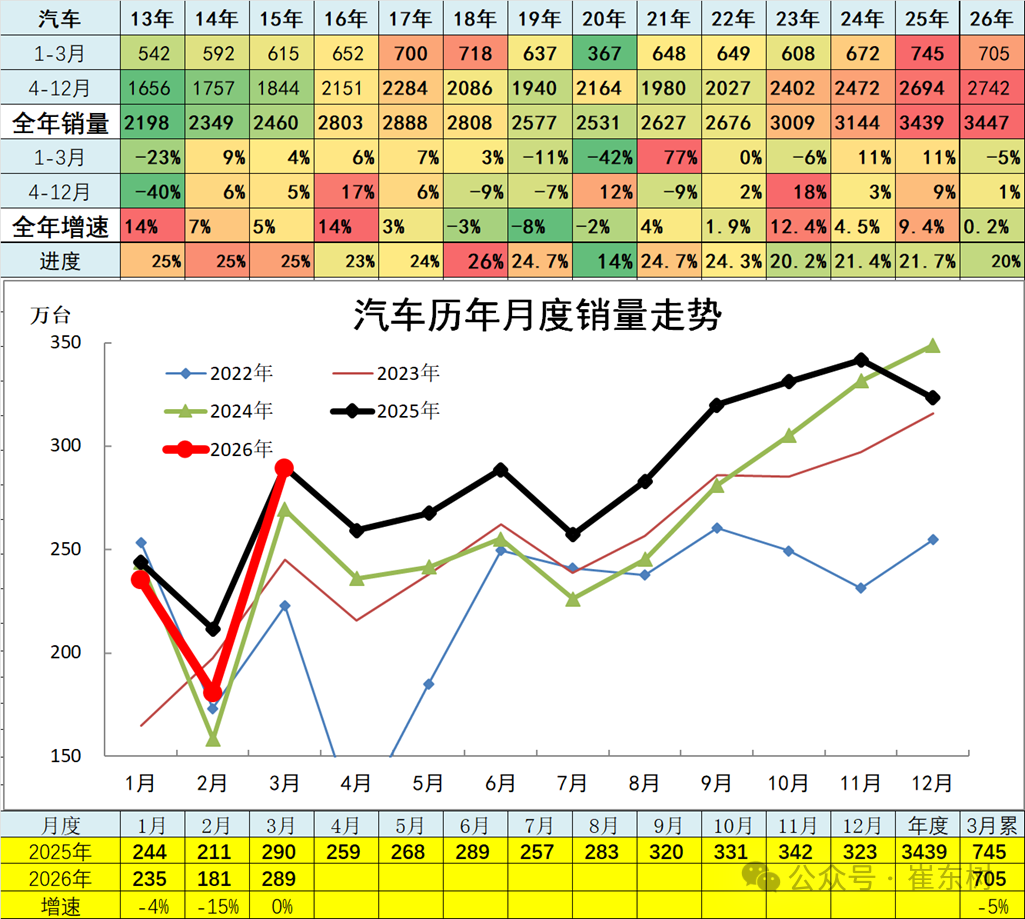

The overall automotive market in 2026 remained stable.

Total automobile sales in March 2026 amounted to 2.89 million units, representing a year-on-year decrease of 0.1%. From January to March 2026, total automobile sales reached 7.05 million units, with a cumulative decline of 5%. The truck market performed strongly, while the passenger car and bus markets were slightly weaker. Exports were strong, but the domestic market was weak. Overall, manufacturer sales trends remained relatively stable.

Total automobile sales in March 2026 amounted to 2.89 million units, representing a year-on-year decrease of 0.1%. From January to March 2026, total automobile sales reached 7.05 million units, with a cumulative decline of 5%. The truck market performed strongly, while the passenger car and bus markets were slightly weaker. Exports were strong, but the domestic market was weak. Overall, manufacturer sales trends remained relatively stable.

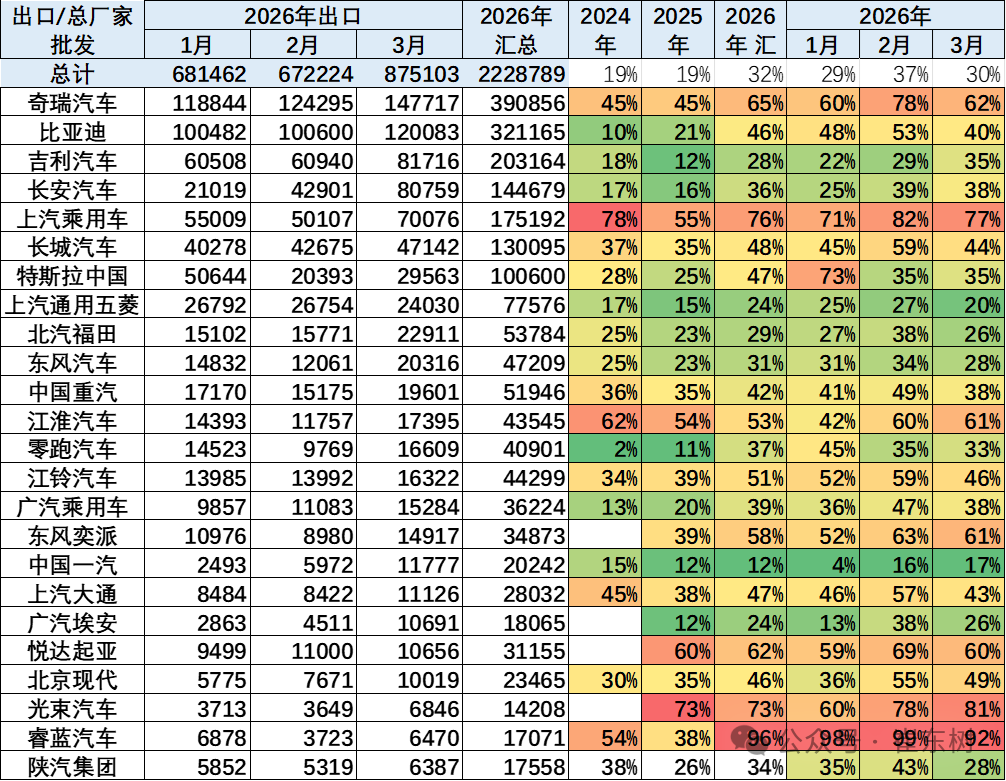

Proportion of exports in total sales

China’s automobile exports have seen explosive growth in recent years. In 2026, exports accounted for 32% of total output, a significant increase from 19% in 2025, making exports a crucial component supporting the growth of China’s automotive industry.

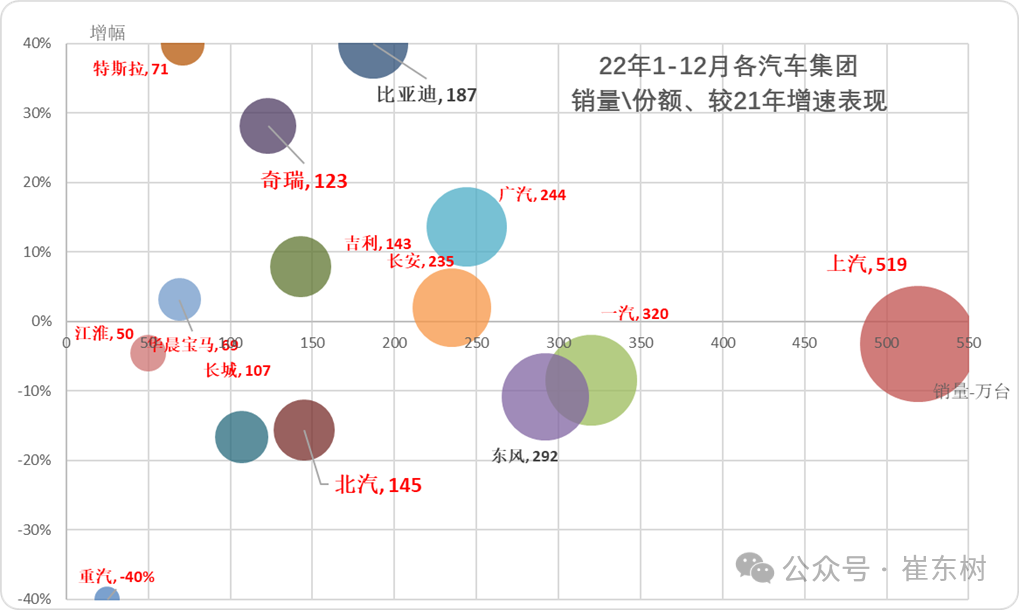

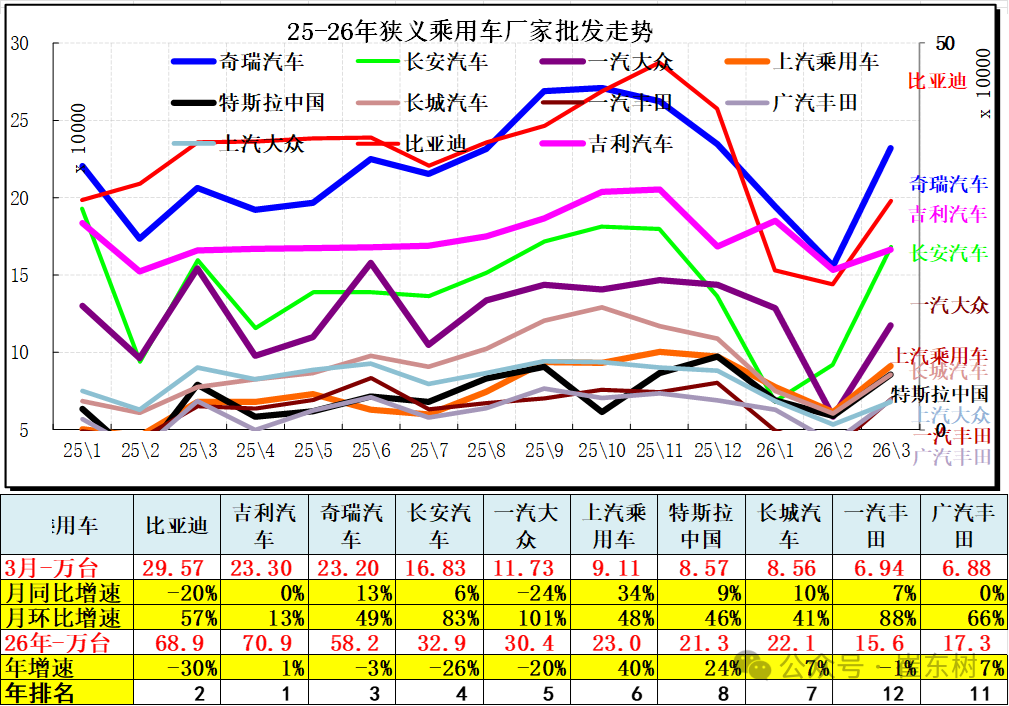

Significant Divergence in the Performance of Major Auto Groups

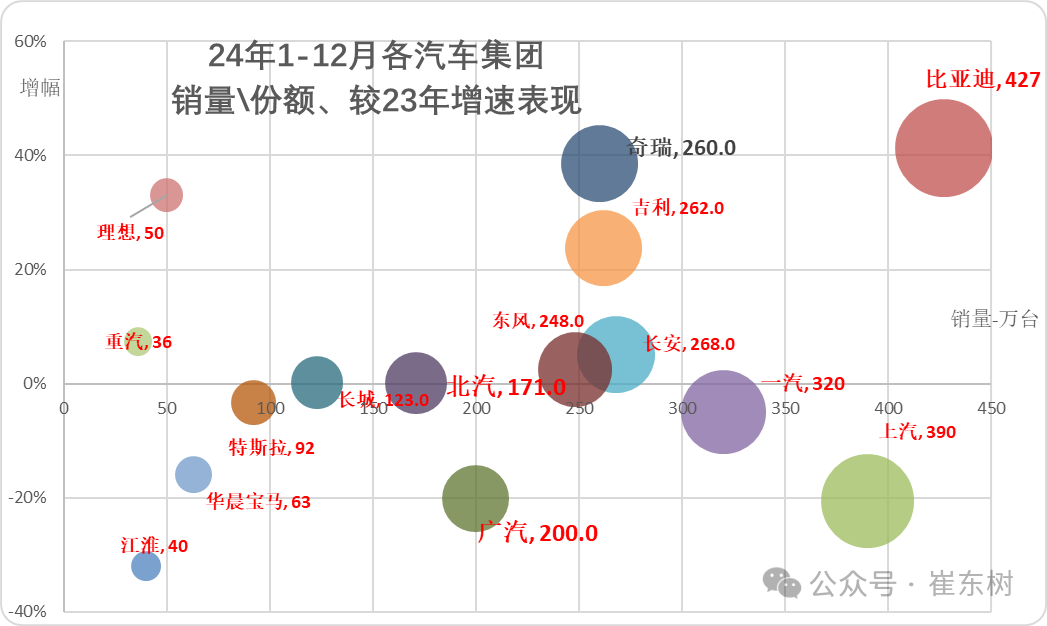

Compared to the chart above from 2021, some automakers performed strongly in 2022, but industry growth rates varied widely. The pandemic at the beginning of 2022 put significant pressure on traditional automakers, especially compounded by the impact of new energy vehicles and the pandemic. State-owned large groups saw mixed results; Guangzhou Automobile Group (GAC) and Chery performed excellently, with Chery showing strong results in both its commercial vehicle and passenger car segments. Northern automakers such as FAW, Great Wall, and BAIC all faced challenges.

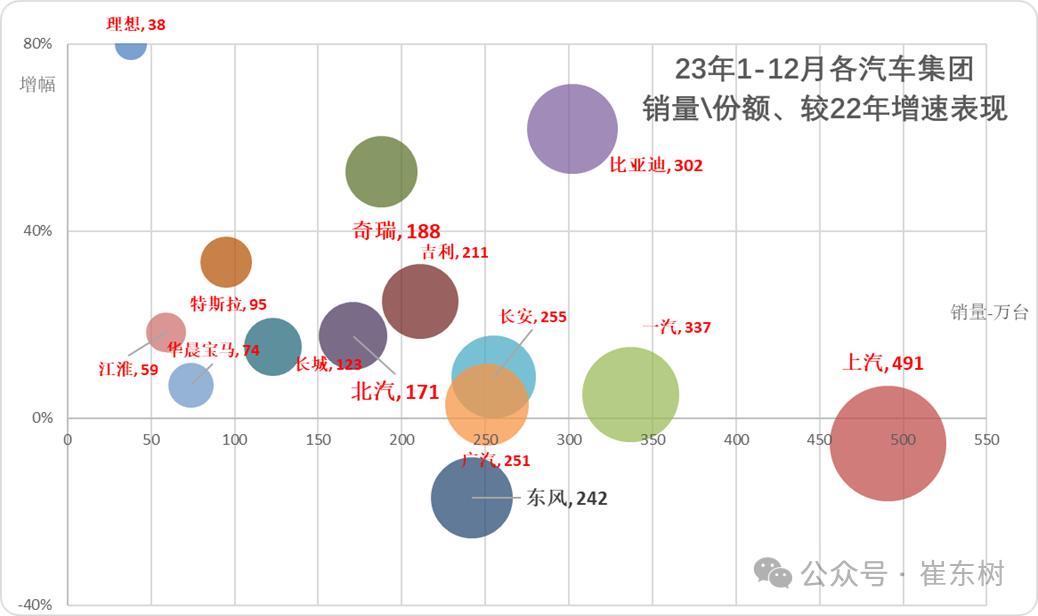

At the beginning of 2023, the promotion of new energy vehicles contributed to the divergence in the auto market trends. The three major state-owned enterprises showed divergent performances, with some falling behind. BYD and other new energy companies performed well, while Chery and Tesla exhibited relatively strong results this year. Second-tier automakers showed mixed performances, as the transition between old and new drivers and the sustained losses in new energy vehicles caused significant downturns among small and medium-sized enterprises, especially in self-owned brands.

The lineup of automotive groups underwent comprehensive changes in 2024. BYD’s new product price cuts boosted volume. Thanks to the booming demand for passenger cars and overseas contributions, Chery, Geely Auto, and Dongfeng performed well, while SAIC continued to experience a sharp decline. Growth rates of new energy vehicles from BYD and Tesla diverged significantly.

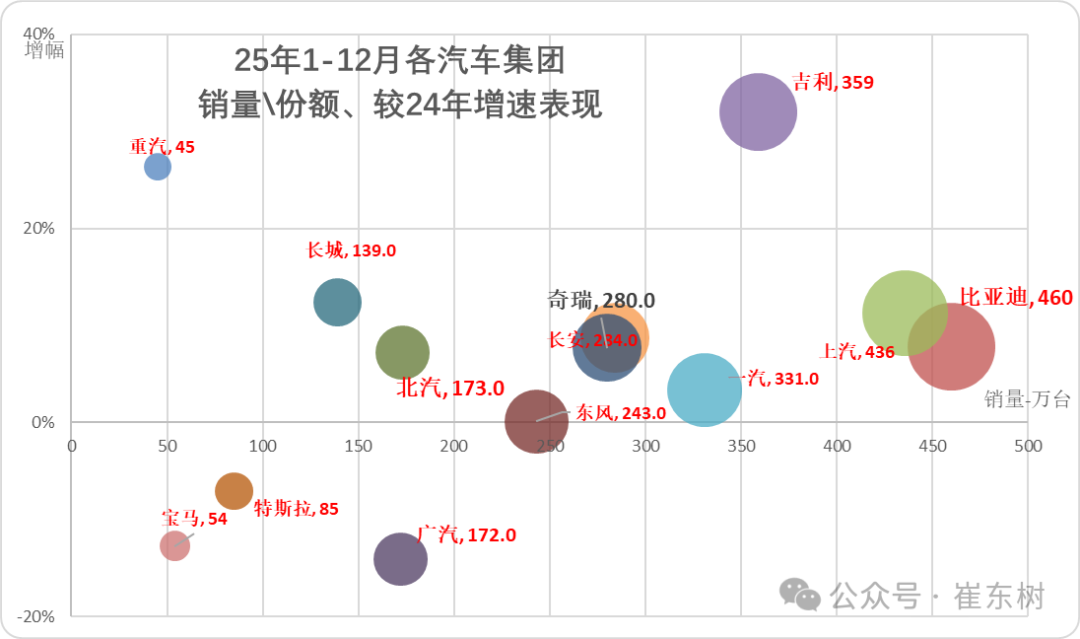

The manufacturer landscape in the auto market underwent dramatic shifts, with sharp differentiation in growth rates. Starting in 2025, private enterprises replaced state-owned enterprises as the main drivers of the industry, with Geely, BYD, Chery, and Great Wall maintaining high growth levels.

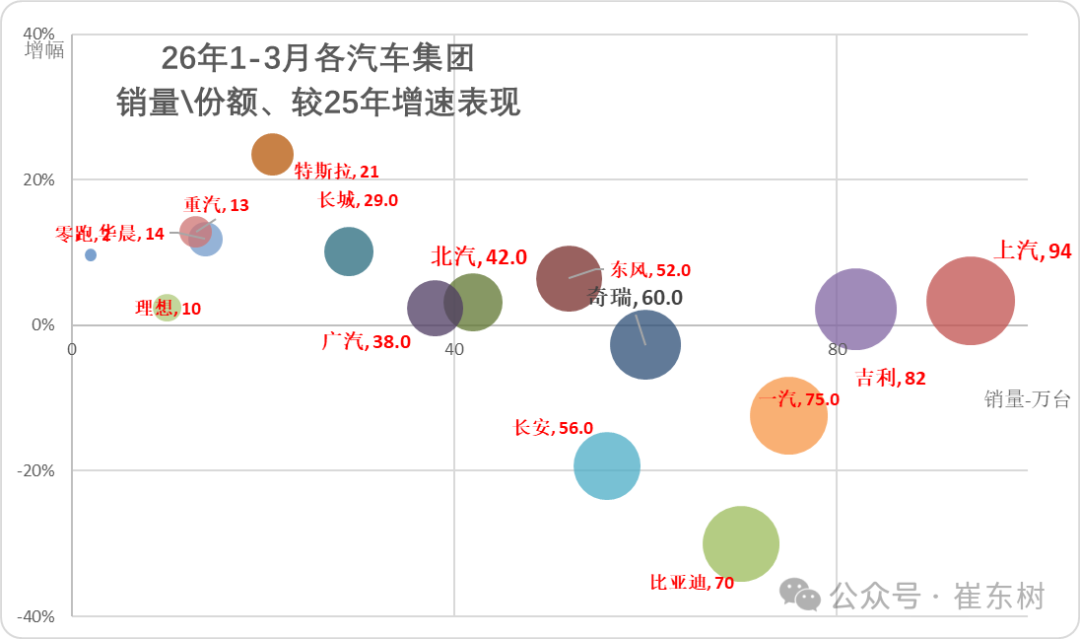

Achieving a strong start in Q1 was a key focus for all companies. Despite a severe and sluggish market, SAIC, Geely, Dongfeng, and BAIC performed strongly from January to March this year, with improved growth rates.

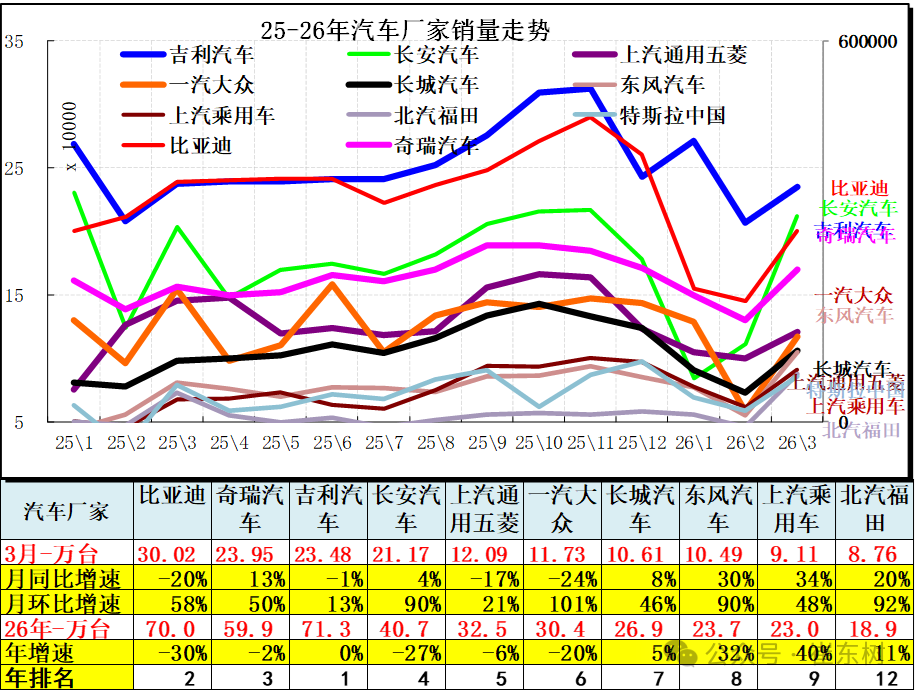

The competitive landscape of automobile manufacturers in 2025 remained relatively stable, with a substantial rise in the status of domestic brands. Although manufacturers’ sales in March were generally good, weak retail performance weighed on passenger vehicle manufacturers. Some manufacturers, like BYD, showed very strong performance compared to February, while SAIC Passenger Cars and Changan Automobile strengthened their year-on-year positions. However, some manufacturers, including BYD, still made significant adjustments to their March sales year-on-year.

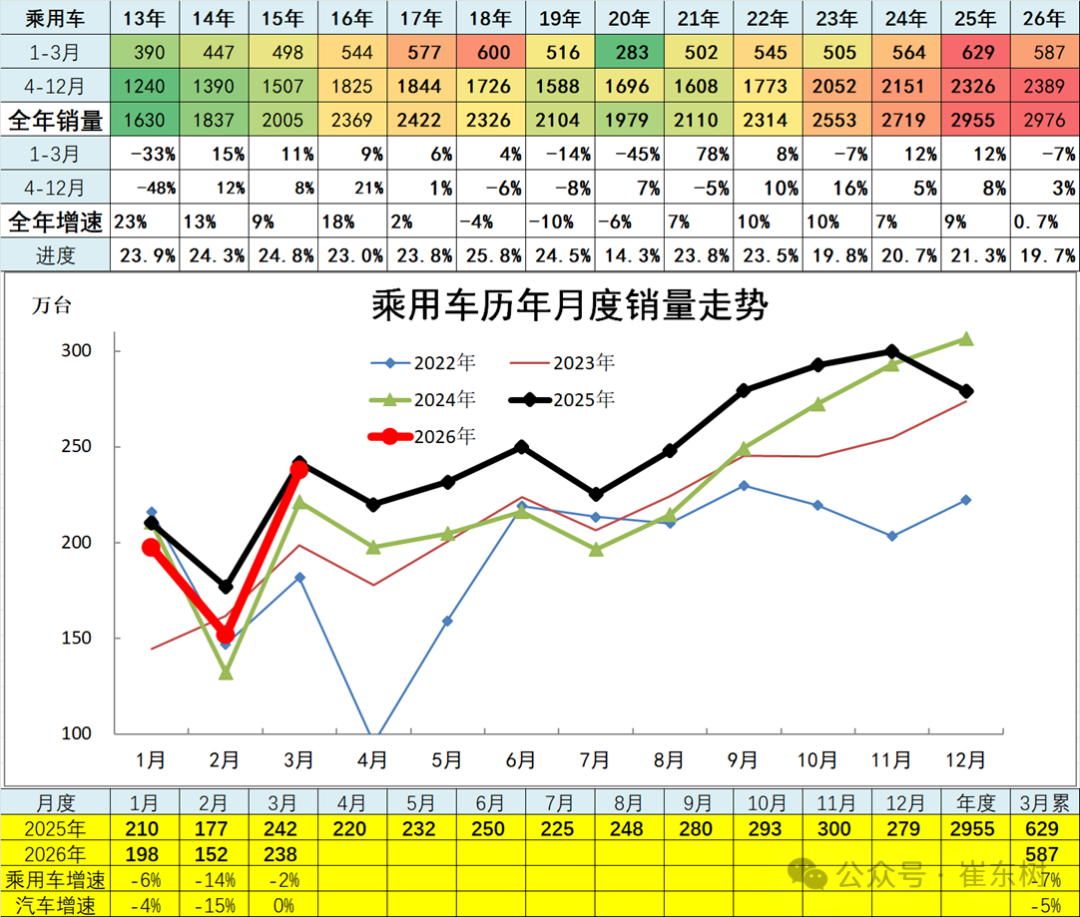

Production and Sales Trends of Narrowly Defined Passenger Vehicle Enterprises

Total narrow-sense passenger vehicle sales in March 2026 amounted to 2.38 million units, representing a year-on-year decrease of 2%. From January to March 2026, total narrow-sense passenger vehicle sales reached 5.87 million units, a year-on-year decrease of 7%. In recent years, technological innovation and the competitiveness of new products in the new energy vehicle sector have grown steadily, whereas the introduction of new fuel-powered models has been lackluster. At the beginning of 2026, new energy vehicles entered an adjustment period, and dealers’ confidence was low, which dampened growth rates.

In March 2026, domestic passenger vehicle manufacturers achieved comprehensive leadership. The performance of major manufacturers was generally weak, while domestic brands performed exceptionally well, and joint venture manufacturers showed a relatively weak trend. BYD took the lead, Geely Auto ranked second, Chery maintained third place in March, and the top three are increasingly closing the gap. Joint ventures such as FAW-Volkswagen and SAIC Volkswagen demonstrated relatively lackluster performance.

The main camp of passenger vehicle manufacturers rapidly differentiated, with export-oriented enterprises and new energy vehicle-focused manufacturers performing strongly. Joint ventures showed particularly evident differentiation, with Toyota standing out.

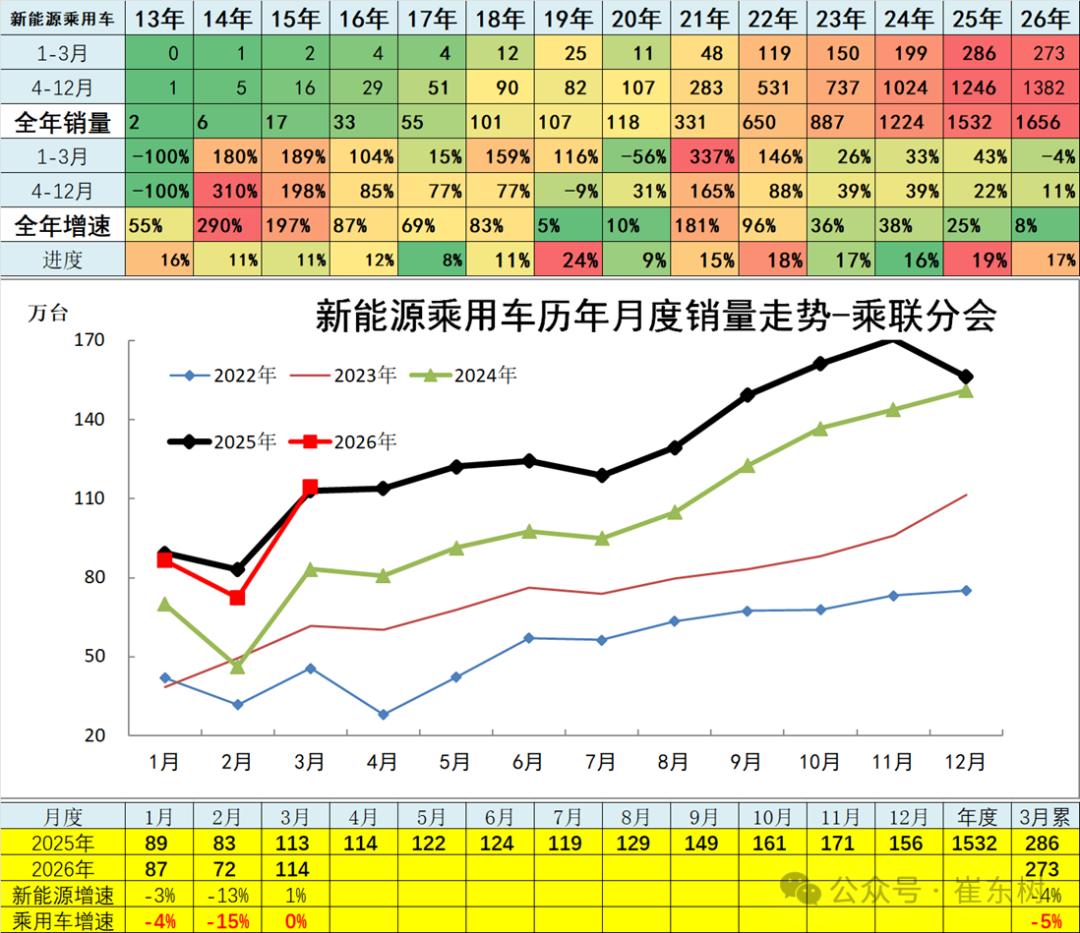

Production and sales trends of new energy passenger vehicle enterprises

In March 2026, the total sales volume of new energy passenger vehicle manufacturers reached 11.4 million units, an increase of 1% year-on-year; from January to March 2026, cumulative sales reached 27.3 million units, marking a year-on-year decline of 4%. The pressure from subsidies for scrapping and updating at the beginning of 2026 was significant, compounded by manufacturers’ price resistance and weak demand for new energy vehicles before the Spring Festival, leading to greater challenges in the domestic market trajectory for new energy vehicles amid sluggish demand.

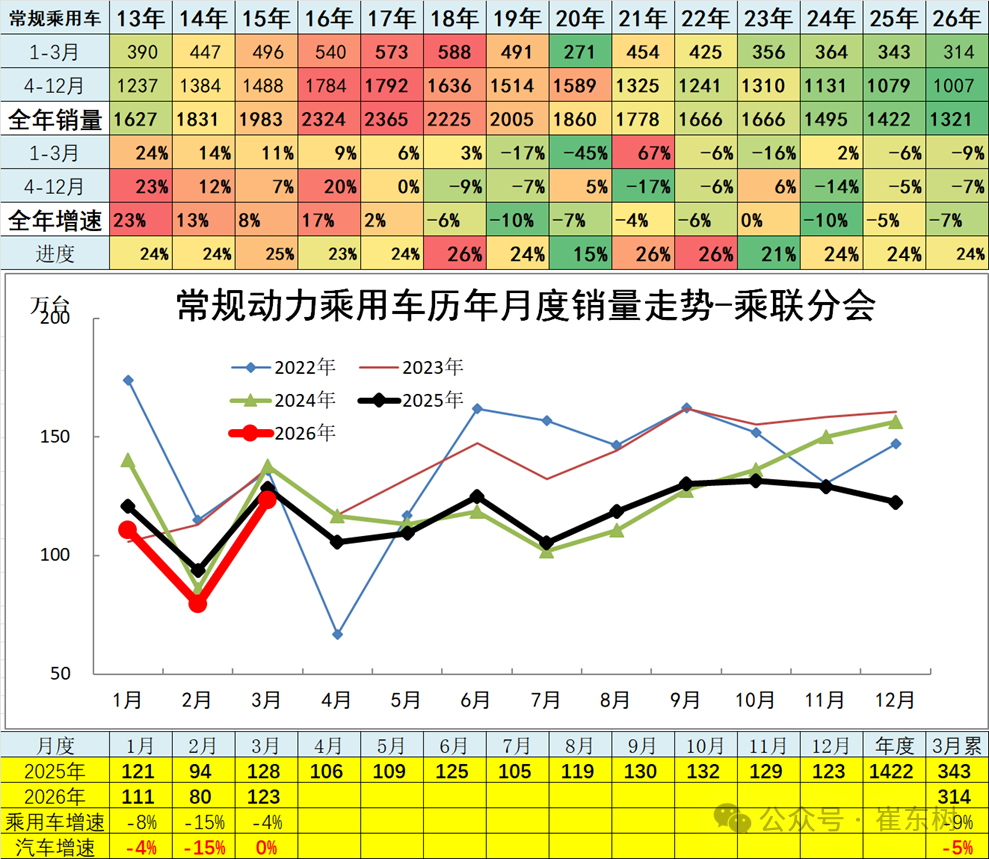

Production and sales trends of traditional power passenger vehicle enterprises

In 2023, the sales volume of traditional fuel narrow-sense passenger vehicles reached 16.66 million units, roughly flat compared to the same period in 2022; in 2024, sales were 14.95 million units, a year-on-year decrease of 10%; in 2025, sales were 14.22 million units, marking a year-on-year decline of 5%; and from January to March 2026, sales reached 3.14 million units, down 9%. With persistently high oil prices, the market trajectory remained weak in 2026.

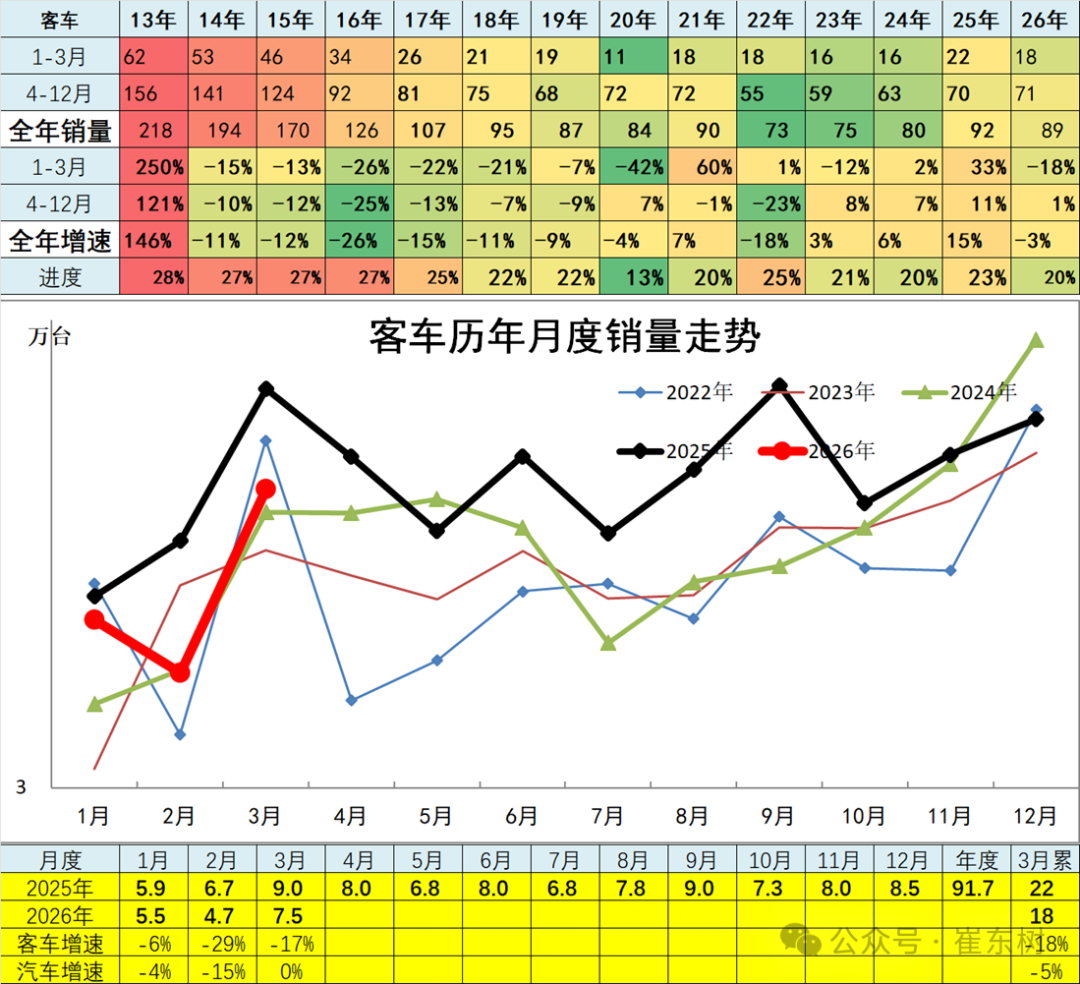

Production and sales classification trends of bus enterprises

In 2023, the cumulative annual sales volume of bus manufacturers totaled 750,000 units, with a cumulative growth rate of 3%; in 2024, cumulative bus sales reached 800,000 units, with a cumulative increase of 6%; in 2025, cumulative bus sales amounted to 920,000 units, reflecting a cumulative growth rate of 15%; and from January to March 2026, bus sales totaled 180,000 units, marking an 18% year-on-year decline. The pulling effect of exports and new energy logistics vehicles remained moderate.

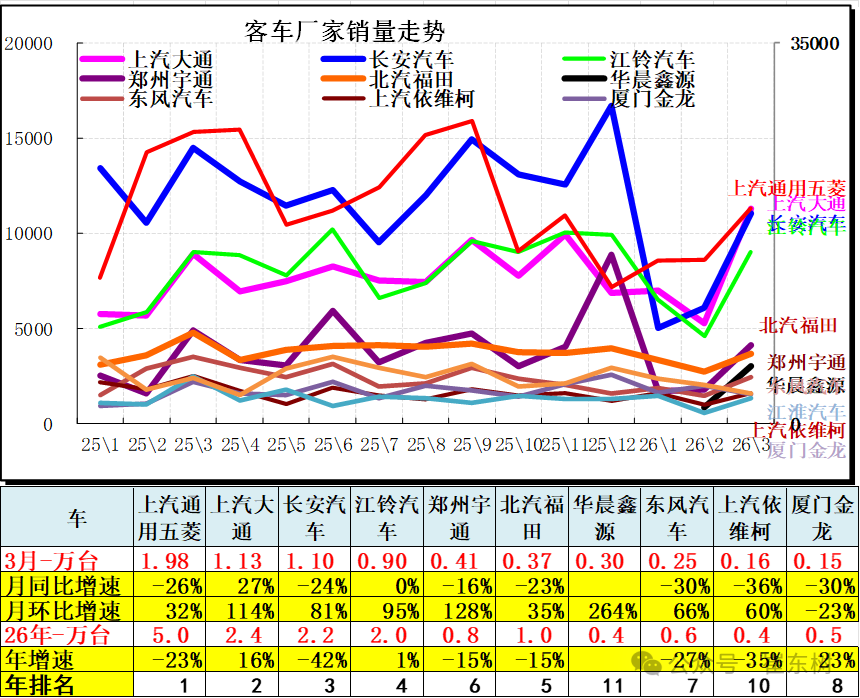

After a year-end surge in 2025, the bus market trajectory relatively declined in 2026. Leading manufacturers such as SAIC Maxus demonstrated strong overall sales in recent months, while SAIC-GM-Wuling performed moderately. Demand for logistics light buses and microbuses fluctuated significantly, with substantial contributions from exports. In 2026, commercial vehicle performance by Jiangling Motors and SAIC Maxus remained favorable, with notable month-on-month recoveries observed in March by Changan, Jiangling, and Yutong.

Production and Sales Classification Trends of Truck Enterprises

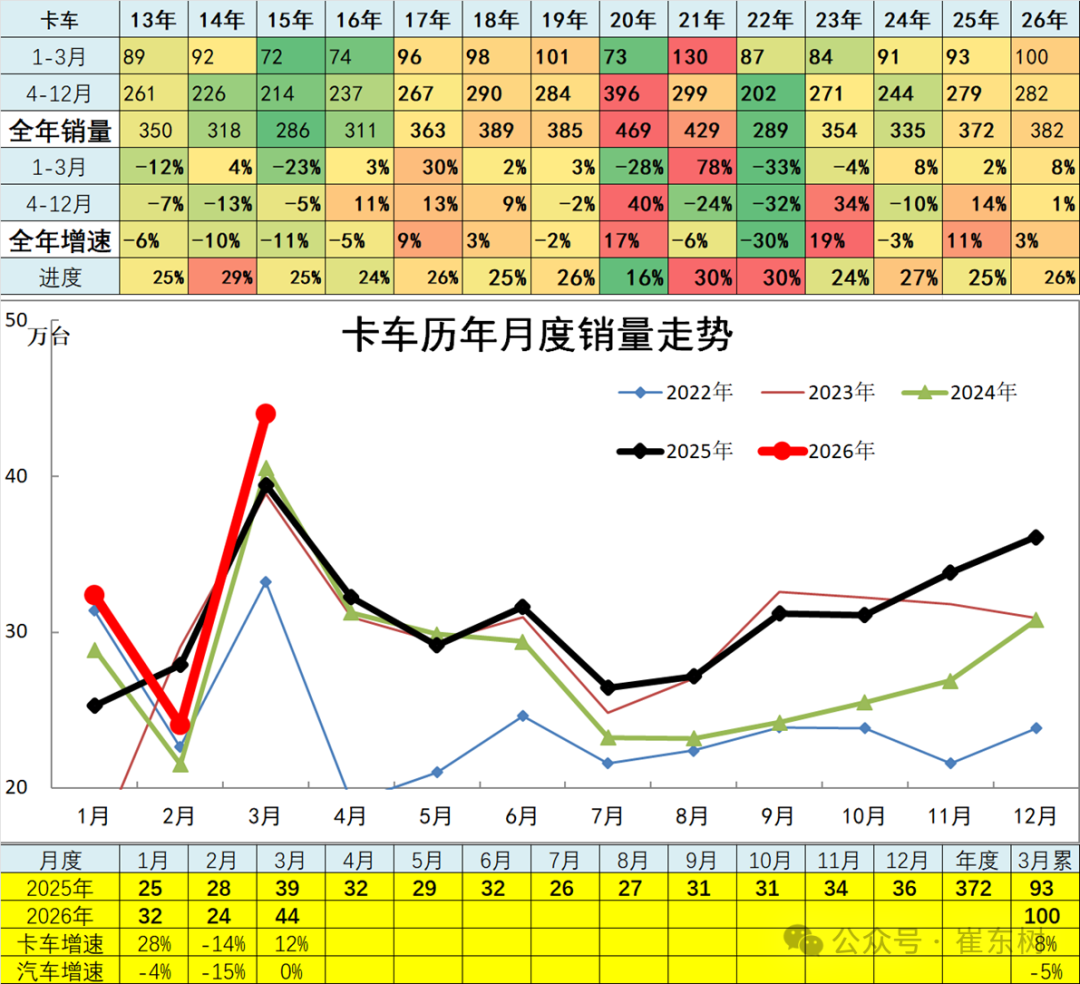

In 2023, the cumulative annual truck sales volume reached 3.54 million units, with a cumulative growth rate of 19%; in 2024, cumulative truck sales were 3.35 million units, reflecting a cumulative decline of 3%; in 2025, truck sales reached 3.72 million units, with a cumulative growth rate of 11%; and from January to March 2026, truck sales totaled 1 million units, representing an 8% year-on-year increase, forming an exceptionally strong growth trend at the beginning of the year.

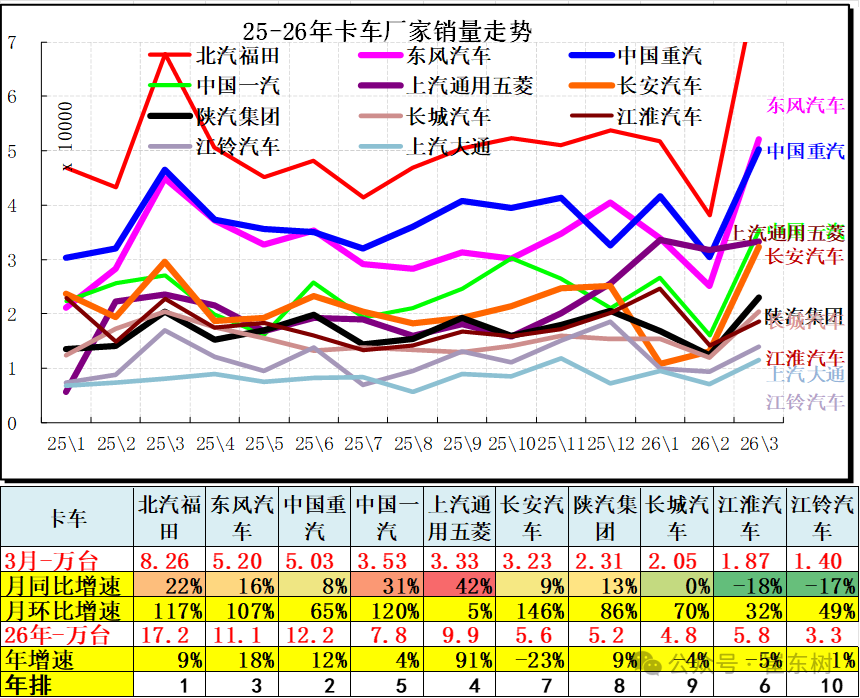

The differentiation among key truck manufacturers became more pronounced in 2026, with leading truck manufacturers demonstrating robust performance. Brands such as Foton, China FAW, Wuling, and Jiangling saw explosive year-on-year growth in March compared to the same month last year.

Heavy-duty trucks experienced a significant increase in January 2026, with electric heavy-duty trucks showing particularly strong performance. FAW, Shanqi, and Sinotruk reported robust growth, while the overall industry structure remained relatively stable.