- In recent days, General Motors confirmed it will revive the Chevrolet Camaro for the 2027/2028 model years, while also expanding its sedan lineup by building the new Camaro, Cadillac CT5, and a returning Buick sedan on a shared second-generation Alpha platform at the Lansing Grand River plant.

- This move marks a clear bet on higher-margin performance and internal combustion vehicles alongside ongoing EV efforts, using a common architecture to improve manufacturing efficiency and broaden the appeal of GM’s legacy brands.

- We’ll now examine how GM’s decision to revive the Camaro on a shared Alpha platform could influence the company’s broader investment narrative.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

General Motors Investment Narrative Recap

To own GM, you need to believe it can balance capital‑intensive EV ambitions with profitable trucks and SUVs, while keeping quality and warranty costs under control. The Camaro and new Alpha-platform sedans reinforce GM’s commitment to higher-margin internal combustion products, but they do not materially change the near term focus on EV execution and software monetization, or the key risk that elevated warranty and quality issues, including recent recalls, could pressure margins and brand perception.

In this context, GM’s plan to revive the Camaro, share its Alpha 2 platform with the Cadillac CT5 and a returning Buick sedan, and consolidate production at Lansing Grand River is particularly relevant. It shows GM continuing to invest in performance and premium ICE offerings alongside its EV push, which matters for near term earnings power and cash generation that can support ongoing buybacks, dividends, and the heavy spending required for EVs and software.

But beneath the excitement around a new Camaro, investors should also be aware of the ongoing risk that higher warranty and software costs could…

Read the full narrative on General Motors (it’s free!)

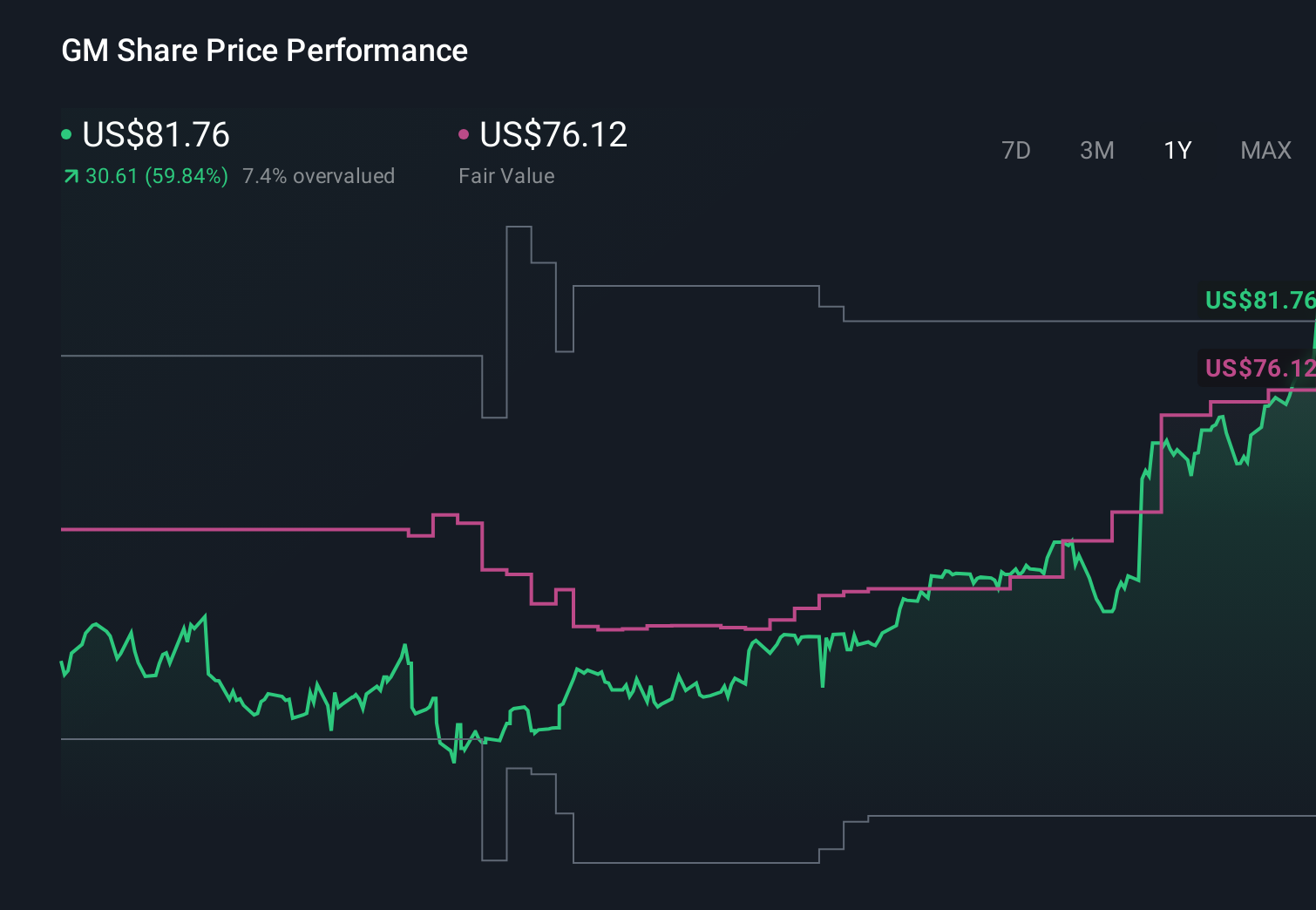

General Motors’ narrative projects $185.3 billion revenue and $8.0 billion earnings by 2028. This implies a 0.4% yearly revenue decline but an earnings increase of about $1.5 billion from $6.5 billion today.

Uncover how General Motors’ forecasts yield a $79.46 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue around US$187.9 billion and earnings of US$9.9 billion by 2029, and the Camaro news could either soften their concern about reliance on trucks and SUVs or deepen worries about EV delays depending on how you view the trade off.

Explore 8 other fair value estimates on General Motors – why the stock might be worth as much as 57% more than the current price!

Reach Your Own Conclusion

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

No Opportunity In General Motors?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com