- In late March 2026, VinFast expanded its EV lineup with the VF 9, a fully electric three-row SUV in Canada starting at C$77,308, featuring up to 518 km of range, 402 horsepower, and extensive 10-year warranties on both vehicle and battery.

- The VF 9’s combination of family-focused space, premium in-cabin features such as second-row massage seats and Sony RIDEVU entertainment, and broad charging and roadside-support services highlights VinFast’s push to position itself as a full-service EV provider rather than just a vehicle manufacturer.

- Now we’ll examine how this family-oriented VF 9 launch, with its long-range and extensive warranty, could reshape VinFast’s investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 36 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

VinFast Auto Investment Narrative Recap

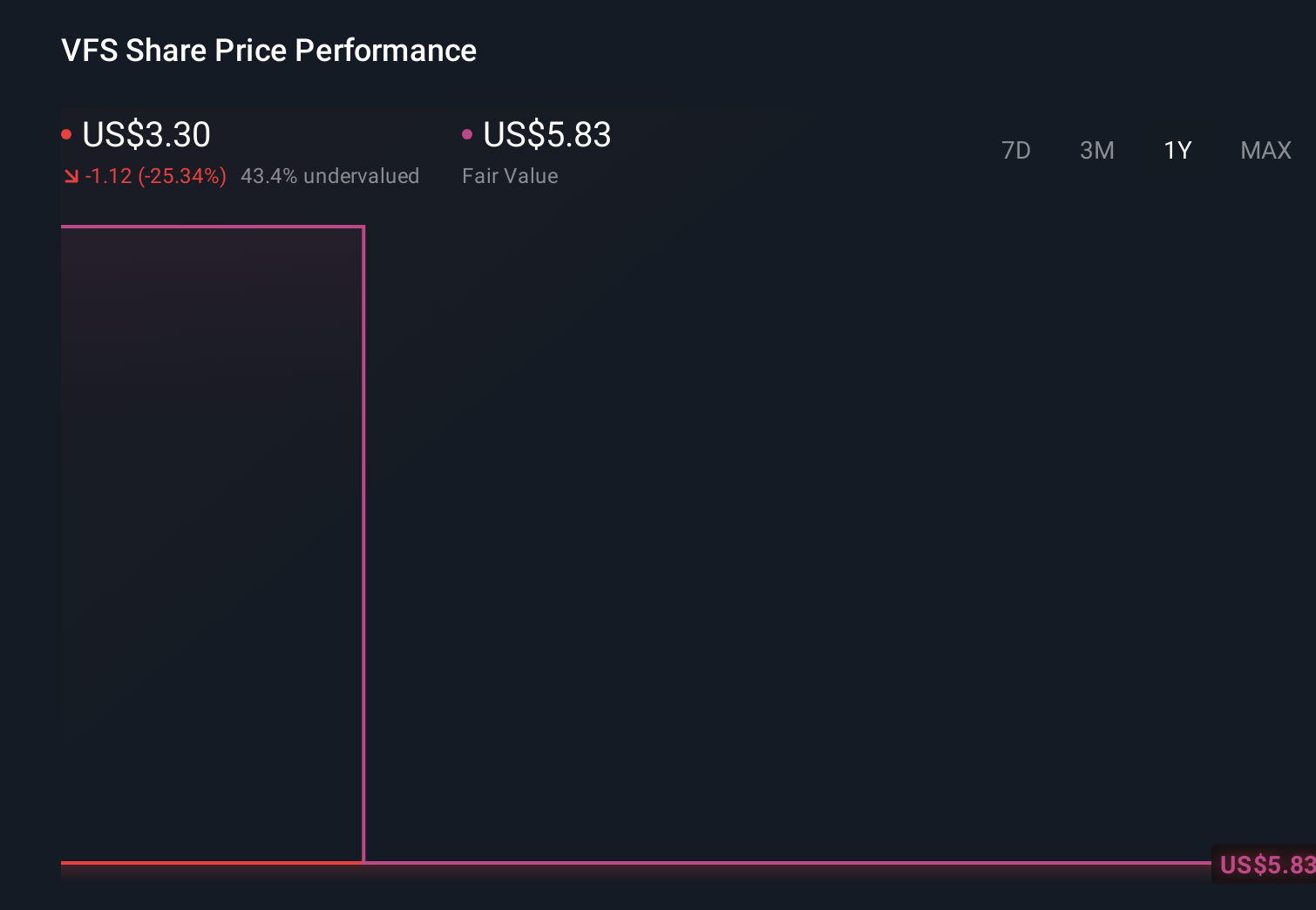

To own VinFast, you need to believe it can grow from a loss-making challenger into a trusted global EV brand while managing high cash burn and limited liquidity. The VF 9’s Canada launch reinforces VinFast’s full-service positioning, but does not materially change the near term catalyst, which remains its ability to scale deliveries without deepening losses. The biggest immediate risk is whether heavy spending and negative gross margins can be reduced before fresh capital is required.

The most relevant recent announcement alongside the VF 9 news is VinFast’s 2026 delivery target of 300,000 EVs globally, with emphasis on Asia. That ambition frames the VF 9 as one piece of a much broader volume push across regions and segments, where success could help support revenue growth but also increase pressure on costs and execution if demand or pricing do not meet expectations.

Yet behind the long warranties and premium features, there is a key liquidity risk investors should be aware of…

Read the full narrative on VinFast Auto (it’s free!)

VinFast Auto’s narrative projects ₫239006.9 billion revenue and ₫5540.6 billion earnings by 2029.

Uncover how VinFast Auto’s forecasts yield a $6.30 fair value, a 50% upside to its current price.

Exploring Other Perspectives

While consensus focuses on VF 9 execution risk, the most optimistic analysts see a very different story, with revenue once expected to grow about 41% a year and earnings potentially reaching roughly ₫9,301.1 billion; if that sounds ambitious beside VinFast’s cash burn and concentration in Vietnam, it is exactly why you should compare several viewpoints before deciding what you believe this latest launch might change.

Explore 5 other fair value estimates on VinFast Auto – why the stock might be a potential multi-bagger!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Seeking Other Investments?

Don’t miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com