- Li Auto Inc. reported that it delivered 30,895 vehicles in June 2026, bringing cumulative deliveries to 1,733,687 vehicles by mid‑year.

- Despite celebrating this production milestone and rolling out new models like the Li L8 flagship SUV, Li Auto is contending with weaker vehicle margins and consecutive monthly delivery declines.

- Next, we’ll examine how these softer margins and falling deliveries may reshape Li Auto’s investment narrative built around technology and expansion.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

Li Auto Investment Narrative Recap

To own Li Auto today, you need to believe its technology heavy, BEV focused roadmap and software ambitions can offset current delivery softness and weaker vehicle margins. The June delivery figure confirms pressure on near term growth, which keeps the key catalyst centered on whether new models like the Li L8 and upcoming Li L6 can stabilize volumes. The biggest risk right now is that rising competition and price pressure keep margins subdued for longer, straining already negative free cash flow.

The most relevant recent announcement here is Li Auto’s Q2 2026 guidance, which calls for 95,000 to 100,000 deliveries and revenue of RMB 24.1 to 25.4 billion, both down year over year. This guidance, combined with June’s delivery weakness, ties directly into the central catalyst of a successful model transition and the risk that price competition and incentives compress margins further, just as the company commits to heavy AI and BEV investment.

Yet behind the product milestones and charging build out, the real pressure point investors should be watching is how sustained price competition could…

Read the full narrative on Li Auto (it’s free!)

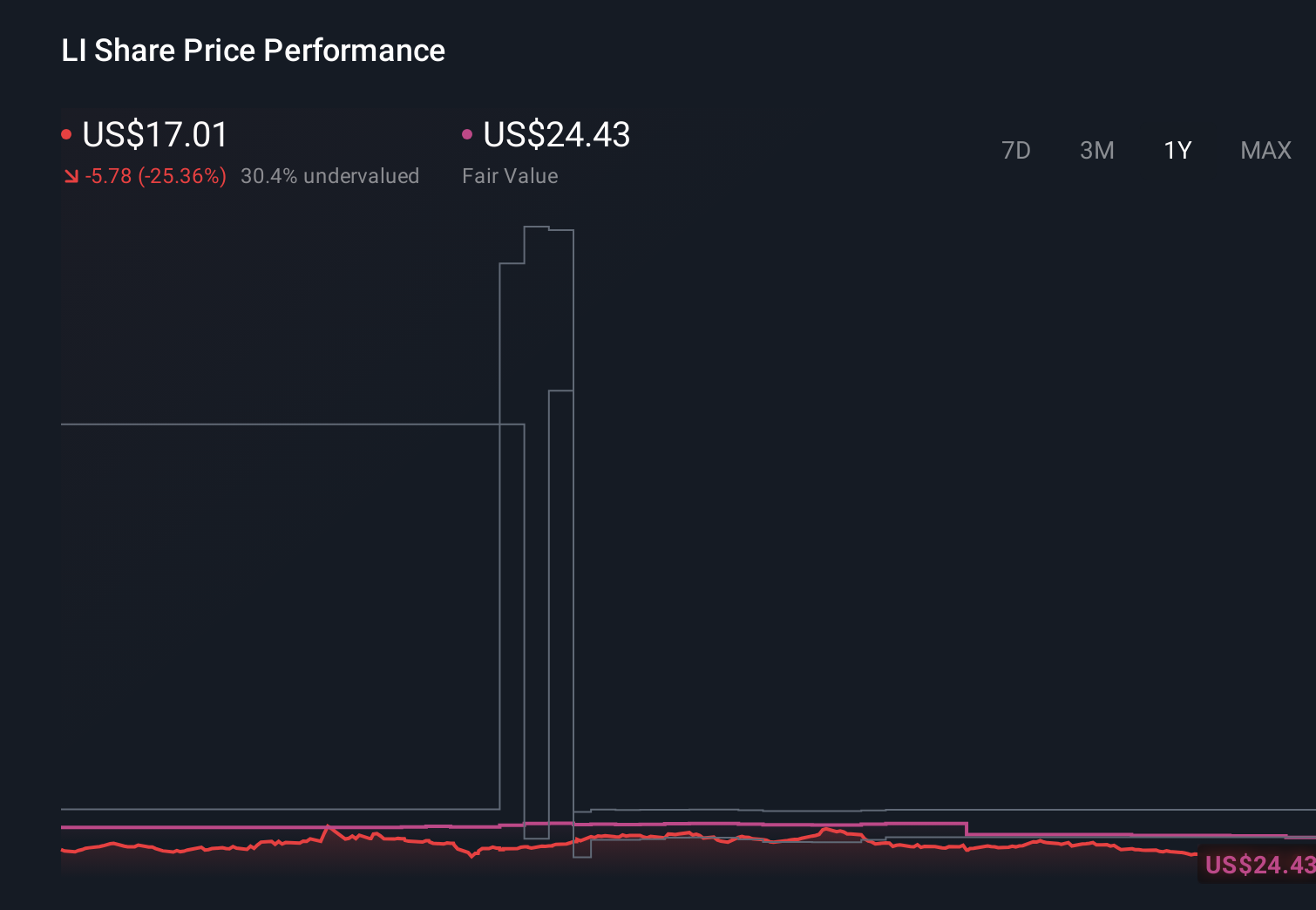

Li Auto’s narrative projects CN¥168.5 billion revenue and CN¥7.6 billion earnings by 2029. This requires 15.5% yearly revenue growth and a CN¥9.4 billion earnings increase from -CN¥1.8 billion today.

Uncover how Li Auto’s forecasts yield a $18.55 fair value, a 53% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts once modeled roughly 30 percent annual revenue growth and earnings of about CN¥15.6 billion by 2029, yet June’s weaker deliveries and margin pressure highlight how views can diverge sharply and may need revisiting as you weigh these upside stories against the risk that intensifying price competition keeps chipping away at future profits.

Explore 5 other fair value estimates on Li Auto – why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

- A great starting point for your Li Auto research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Li Auto research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Li Auto’s overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com